One of the most consistent things I observe with buyers (whether they are purchasing their first home in Dubai or adding to an investment portfolio) is that the financing framework catches them off guard.

Not necessarily because it is complicated, because honestly it isn’t once it’s been explained clearly. But most people enter the conversation focused solely on the property: the area, the view, the price per square foot. The mortgage rules feel like a detail to sort out later, after the decision has been made.

That is precisely where the space is left for surprises to happen.

In 2026, Dubai’s mortgage landscape is well-structured and, in many respects, genuinely accessible, but only if you understand the framework before you start looking. The Central Bank of the UAE sets hard caps on how much a bank can lend. Those caps vary by your residency status, the property type, and the purchase price. They don’t negotiate. And in a market where mortgage-backed transactions grew 23% year-on-year in Q4 2025, understanding the rules isn’t optional, it’s the starting point.

In this article, I will walk through what the rules actually say, what they mean in practice, and what they signal differently for end-users versus investors.

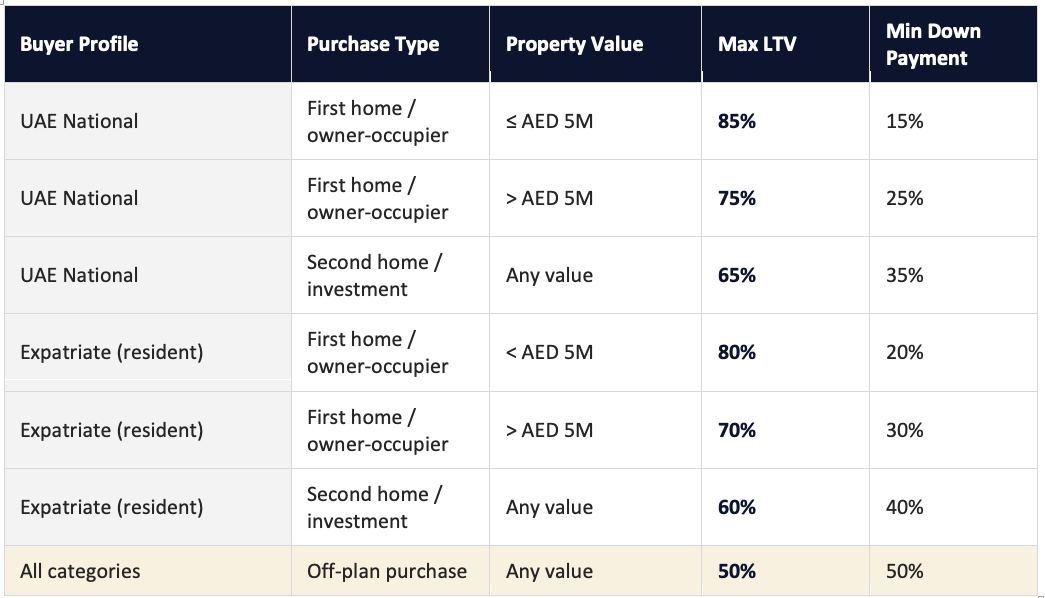

Loan-to-Value Framework: How Much a Bank Will Actually Lend You

The Central Bank of the UAE regulates mortgage lending through Loan-to-Value ratios; the percentage of a property’s assessed value that a bank is permitted to finance. Everything else flows from this number.

Here is how the framework sits in 2026:

A few things worth pausing on here.

First, the LTV is applied to the bank’s valuation of the property, not necessarily the agreed purchase price. If you agree to pay AED 2.1 million and the bank’s valuer assesses the property at AED 1.9 million, the LTV is applied to AED 1.9 million. That gap (the difference between what you’re paying and what the bank will lend against) must come from your own funds. I’ve seen this catch buyers completely by surprise – particularly in a rising market where negotiated prices are running ahead of formal valuations.

Secondly, the off-plan cap of 50% applies to all buyers regardless of nationality, residency, property value, or purchase purpose. No exceptions. This is a structual feature of the market, not bank-by-bank policy, and it has a significant downstream effect on how investors approach new launches, which I’ll come to shortly.

AED 5 Million Breakpoint Every Buyer Should Know About

There is a specific dynamic in Dubai’s mortgage market that in my opinion doesn’t get discussed enough: the cliff edge at AED 5 million.

For resident expats buying below AED 5 million, the maximum LTV is 80%. Above that threshold, it drops to 70%. For a property priced at AED 4.9 million, your required equity is AED 980,000. For a property priced at AED 5.1 million, it becomes AED 1,530,000.

That is an additional AED 550,000 in required cash for a AED 200,000 increase in purchase price.

In practice, this creates something interesting in the secondary market: a large cluster of listings priced just below AED 5 million. Why? Because sellers and agents are aware of the breakpoint. Buyers who understand it are in a stronger negotiating position on properties that sit just above it.

And honestly? It also shapes the advisory conversation I have with clients who are stretching toward a higher-value property. Sometimes the most financially intelligent decision isn’t to push slightly above a threshold. It’s to find the right asset slightly below it and deploy the equity difference elsewhere.

The same breakpoint applies to UAE Nationals, where the LTV moves from 85% below AED 5 million to 75% above it.

Most mortgage mistakes in Dubai are not rate mistakes. They are constraint mistakes, buying the property before understanding the rules.

Off-Plan Financing: Why Developer Payment Plans Exist

Here is something the data makes very clear: off-plan remains structurally penalised by the financing rules. And understanding why explains a lot about how new launches are structured.

Banks will lend a maximum of 50% against an off-plan purchase, for any buyer, regardless of profile. In reality, many major banks apply even stricter internal criteria and prefer not to lend on off-plan at all, particularly from smaller developers. As one report I read recently put it simply: ‘off-plan remains structurally penalised by financing rules, which is why developer payment plans dominate new launches.’

That is exactly right. When a developer offers a 60/40 or 70/30 payment plan, where 60 or 70% is paid during construction and the balance on handover, they are effectively compensating for the fact that bank financing isn’t viable for most buyers. The payment plan replaces the mortgage.

For investors, this is worth internalising. Off-plan with a structured payment plan can be highly capital-efficient: you are deploying equity in tranches rather than committing the full purchase price upfront. But the trade-off is that you are effectively your own financier during the construction period, and the return on that capital is entirely dependent on delivery, market conditions at handover, and rental demand in the community once it matures.

The rule of thumb I give clients: off-plan with a reputable master-developer and a clear payment schedule is a fundamentally different risk profile from off-plan with a smaller developer on a compressed timeline.

To be clear: the financing rules don’t distinguish between the two. Your due diligence has to.

Fixed or Variable in 2026: The Rate Question

Most UAE mortgages are priced as EIBOR, the Emirates Interbank Offered Rate, plus a bank margin. As of Q1 2026, EIBOR sits at approximately 4.6%. Banks are adding margins of between 1.25% and 3.25% depending on the borrower’s profile and the property, putting variable-rate mortgages in the range of approximately 5.85% to 6.2%.

Fixed-rate products currently start from around 3.99% to 4.2% for initial periods of one to three years, meaningfully below the variable equivalent. Banks are competing aggressively on fixed-rate offerings right now, and for most buyers I work with, the fixed option represents genuine payment certainty during a period when you want to establish cashflow before re-evaluating.

One thing that often goes unsaid: ‘fixed rate’ in Dubai typically means fixed for an introductory window, commonly one to five years, after which the mortgage reverts to a variable EIBOR-linked rate. You are not locking in for the full tenure. What you are doing is buying yourself a period of certainty while the rate environment settles.

My honest view: for end-users buying a home they plan to live in, the current fixed rate products are attractive. For investors modelling rental yield against mortgage repayments, understanding what happens at the fixed-to-variable transition is part of the underwriting, not an afterthought.

The Affordability Gate: Debt Burden Ratio (DBR)

Beyond LTV, the Central Bank of the UAE imposes a second hard constraint: the Debt Burden Ratio, or DBR. This caps your total monthly debt obligations, including the proposed mortgage, at 50% of your gross monthly income.

The bank isn’t asking whether you can afford the payment under today’s rate. It is stress-testing your capacity under a higher rate, while carrying all existing obligations, inside that 50% ceiling. The CBUAE regulation requires banks to stress test at 2 to 4 percentage points above the current rate depending on where we are in the interest rate cycle. In practice, this means your full financial picture matters: car loans, personal loans, credit card limits, and any overseas obligations all feed into the calculation.

There is also a maximum financing amount: seven times annual gross income for expatriates, eight times for UAE nationals. For a resident expat earning AED 30,000 per month, AED 360,000 annually, the ceiling is AED 2.52 million in total loan value. At an 80% LTV, that supports a property purchase of up to approximately AED 3.15 million, assuming no existing debts.

I find this calculation genuinely useful to work through with buyers early. It reframes the conversation from ‘what can I afford to buy’ to ‘what can I afford to borrow’, which is the right question to start with.

End-Users and Investors: Two Different Reads on the Same Rules

The mortgage framework above applies equally to everyone, but it means different things depending on why you are buying.

For end-users, the key takeaway is access. If you are a resident expat buying your first home under AED 5 million, 80% LTV is genuinely generous by regional and global standards. The combination of that leverage, current fixed rates starting below 4.2%, and a 25-year maximum tenure creates a monthly repayment structure that is, for many buyers, more financially logical than continuing to rent. I’ve worked with families who had been renting in Dubai for years, assuming ownership was financially out of reach, and discovered that the maths told a very different story once we mapped it out.

For investors, the calculation is more nuanced. The off-plan financing restriction effectively steers most investment capital toward developer payment plans rather than bank leverage. That isn’t necessarily a problem, a well-structured payment plan from a Tier 1 developer can be as capital-efficient as a mortgage and carry less interest-rate exposure. But it means the investor’s evaluation framework needs to be different: instead of asking ‘what will my mortgage cost relative to rental yield’, the question becomes ‘what is my actual cash outflow schedule and what yield do I need to hit to make this work at handover.’

For investors buying in the ready market, financing is more accessible, 60 to 65% LTV for non-residents, up to 80% for resident expats, and the case for using leverage depends entirely on how the yield stacks up against the cost of debt. At current rates, a property generating 7% gross yield financed at 75% LTV against a 4.5% mortgage rate produces a healthy positive spread. At 5.5% gross yield, the margin compresses significantly. The maths matters.

What to Take Into Your Next Property Conversation

Dubai’s mortgage rules in 2026 are not designed to restrict the market. In my experience, they are designed to protect it, to prevent the kind of overleveraged buying that creates systemic risk in other real estate markets. The LTV caps, the DBR ceiling, the off-plan restrictions: they are conservative by intent, and that conservatism is part of what makes Dubai’s market as stable as it is.

What they require from buyers is preparation. The framework isn’t complicated, but it does need to be understood before you start viewing properties, not after you’ve made an emotional decision about a specific unit.

Know your residency status and what LTV it gives you. Know whether you are buying ready or off-plan and what financing options that creates. Know your DBR position before walking into a pre-approval conversation. And if you are an investor, run the yield-versus-cost-of-debt calculation honestly, including the fixed-to-variable rate transition.

Two things can be true at the same time: this market is genuinely accessible to buyers who prepare, and it will frustrate buyers who don’t. The rules haven’t changed that dynamic, they’ve just made it more visible.

If you would like to walk through how the mortgage framework applies to your specific situation, please reach out to me directly at [email protected] or WhatsApp me on +971 58 554 2669.

Data sources: Central Bank of the UAE (CBUAE Circular No. 31/2013, Board Resolution No. 31/2/2020), Dubai Land Department